(Bloomberg) — While a key Federal Reserve liquidity facility is running low, market analysts say the central bank likely will keep shrinking its balance sheet.

Most Read from Bloomberg

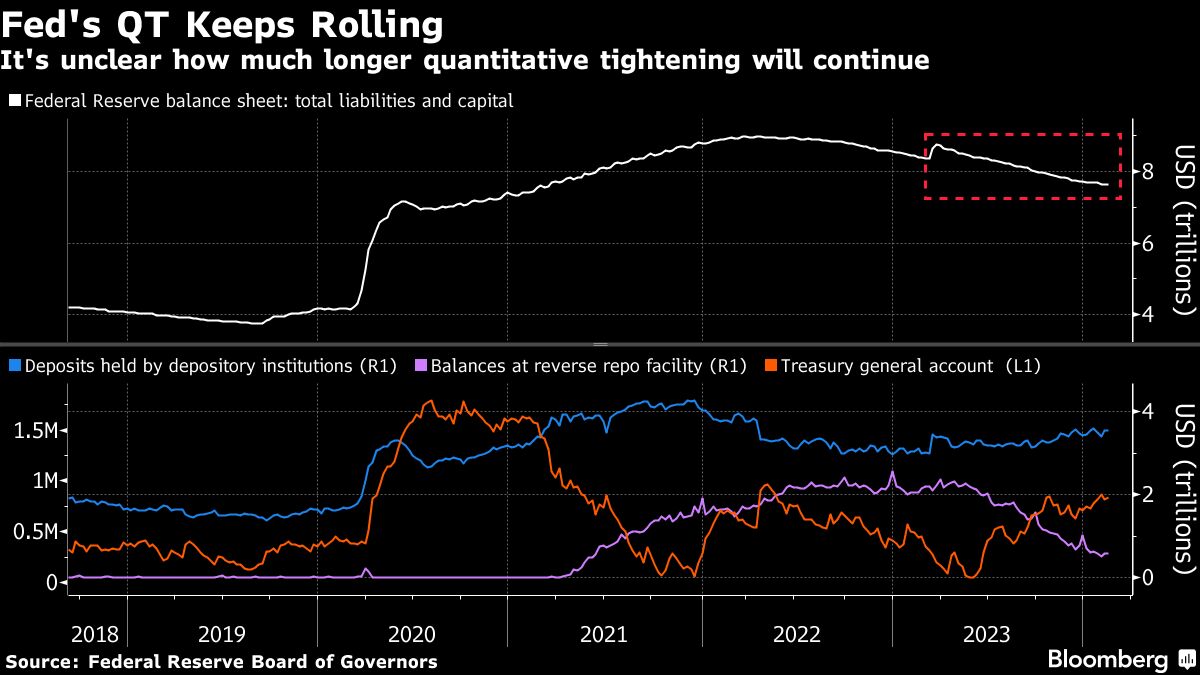

Usage of the Fed’s overnight reverse repurchase agreement facility or RRP — where eligible counterparties can park cash to earn a market rate — briefly dropped below $500 billion last week, continuing a months-long decline.

At the same time, bank reserve balances — another large liability on the central bank’s balance sheet — are $3.54 trillion, according to the latest data. That’s higher than the level seen when the Fed’s asset reduction started in June 2022, a process known as quantitative tightening or QT.

“The surplus outflows from the RRP facility have no place to go except back into reserve balances, where they run the risk of clogging up bank balance sheets,” Wrightson ICAP economist Lou Crandall wrote in a note to clients. “The Fed is likely to view the spillover of surplus cash from the RRP facility into bank reserve accounts as inefficient and a reason to continue to drain liquidity from the financial system in general.”

QT has been in place for more than a year and a half, with the Fed letting as much as $60 billion in Treasuries and as much as $35 billion in agency debt holdings mature each month. But a debate has been simmering over whether the central bank is misjudging how much it can tighten liquidity without creating a scarcity of reserves in the financial system.

Strategists have been trying to determine whether the unwind can continue even after the RRP is empty and how far bank reserves can shrink before they become scarce and cause ructions in the funding markets as happened in September 2019.

Both Barclays Plc and Bank of America Corp strategists have pushed back their timing for the beginning of any QT taper.

Fed Chair Jerome Powell, during last month’s press conference following the Federal Open Market Committee meeting, said that policymakers are planning a more in-depth discussion at the March meeting. He acknowledged that individual members brought up QT tapering during the gathering. Minutes from that meeting will be released on Wednesday.

Yet it’s still unclear how officials view the rapid decline in RRP balances, according to Crandall.

The importance of RRP levels was noted by Dallas Fed President Lorie Logan, who said in January the central bank should slow its balance sheet runoff as reverse repo balances approach a low level. John Williams, her counterpart at the New York Fed, noted last month that bank reserves — a key metric used to guide the unwind — are little changed from the Fed’s pre-QT days.

Overall demand for the RRP has been fading since June, when the Treasury offered an alternative for short-term investors by ramping up fresh bill issuance after the suspension of the debt ceiling. The bill buying accelerated as traders started to bet that the Fed will aggressively cut interest rates this year, spurring money-market funds to further allocate into bills to capture higher yields.

Read more: A $6 Trillion Wall of Cash Is Holding Firm as Fed Delays Cuts

Government money-market funds’ holdings of Treasury bills with maturities longer than 90 days climbed to $489 billion as of Jan. 31 versus $17 billion in March 2022, according to Wrightson ICAP. Even more important has been the expansion of money funds’ private repo market exposure, which surged by another $207 billion last month, according to Office of Financial Research data.

Wrightson’s Crandall said he expects money funds to continue to reduce their reliance on the Fed’s RRP facility in coming months by “aggressively cultivating” these alternative investments.

“If they succeed in doing so, the Fed should be happy to let surplus liquidity continue to run off rather than accumulate in the banking system,” he said.

Most Read from Bloomberg Businessweek

©2024 Bloomberg L.P.