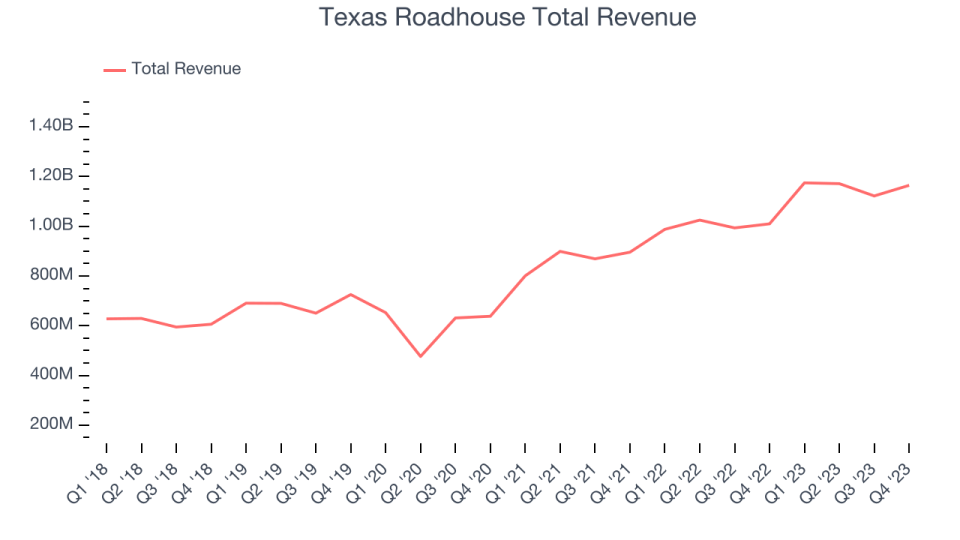

Restaurant company Texas Roadhouse (NASDAQ:TXRH) reported results in line with analysts’ expectations in Q4 FY2023, with revenue up 15.3% year on year to $1.16 billion. It made a GAAP profit of $1.08 per share, improving from its profit of $0.89 per share in the same quarter last year.

Is now the time to buy Texas Roadhouse? Find out by accessing our full research report, it’s free.

Texas Roadhouse (TXRH) Q4 FY2023 Highlights:

-

Revenue: $1.16 billion vs analyst estimates of $1.16 billion (small beat)

-

EPS: $1.08 vs analyst estimates of $1.07 (small beat)

-

Free Cash Flow of $71.11 million, up from $13.19 million in the previous quarter

-

Gross Margin (GAAP): 15.8%, up from 15.1% in the same quarter last year

-

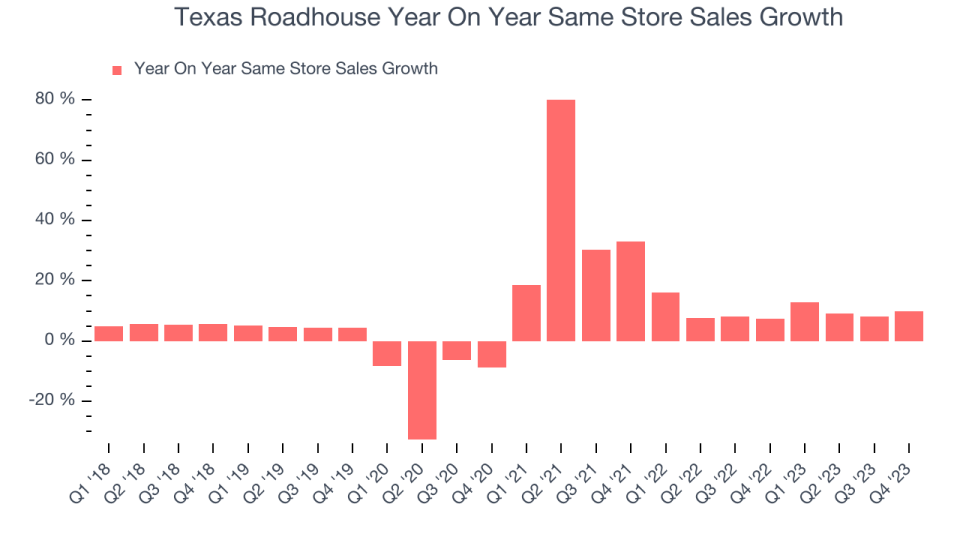

Same-Store Sales were up 9.9% year on year (beat vs. expectations)

-

Same-Store Sales Guidance for 2024: positive growth (reiterated from previous)

-

Store Locations: 741 at quarter end, increasing by 44 over the last 12 months

-

Market Capitalization: $8.84 billion

Jerry Morgan, Chief Executive Officer of Texas Roadhouse, Inc. commented, “We had another outstanding year in 2023, which was highlighted by double-digit same store sales growth and a record number of new system-wide openings across all three brands. We are extremely thankful to our operators for their exceptional leadership and all Roadies who make dining at our restaurants such a legendary experience.”

With locations often featuring Western-inspired decor, Texas Roadhouse (NASDAQ:TXRH) is an American restaurant chain specializing in Southern-style cuisine and steaks.

Sit-Down Dining

Sit-down restaurants offer a complete dining experience with table service. These establishments span various cuisines and are renowned for their warm hospitality and welcoming ambiance, making them perfect for family gatherings, special occasions, or simply unwinding. Their extensive menus range from appetizers to indulgent desserts and wines and cocktails. This space is extremely fragmented and competition includes everything from publicly-traded companies owning multiple chains to single-location mom-and-pop restaurants.

Sales Growth

Texas Roadhouse is one of the larger restaurant chains in the industry and benefits from a strong brand, giving it customer mindshare and influence over purchasing decisions.

As you can see below, the company’s annualized revenue growth rate of 13.9% over the last four years (we compare to 2019 to normalize for COVID-19 impacts) was impressive as it added more dining locations and increased sales at existing, established restaurants.

This quarter, Texas Roadhouse’s year-on-year revenue growth clocked in at 15.3%, and its $1.16 billion in revenue was in line with Wall Street’s estimates. Looking ahead, Wall Street expects sales to grow 11.7% over the next 12 months, a deceleration from this quarter.

Today’s young investors likely haven’t read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Same-Store Sales

Same-store sales growth is a key performance indicator used to measure organic growth and demand for restaurants.

Texas Roadhouse’s demand has outpaced the broader restaurant sector over the last eight quarters. On average, the company has grown its same-store sales by a robust 10% year on year. This performance suggests its steady rollout of new restaurants could be beneficial for shareholders. When a company has strong demand, more locations should help it reach more customers seeking its meals.

In the latest quarter, Texas Roadhouse’s same-store sales rose 9.9% year on year. This growth was an acceleration from the 7.1% year-on-year increase it posted 12 months ago, which is always an encouraging sign.

Key Takeaways from Texas Roadhouse’s Q4 Results

This is a prime example of a quarter that shows a company is staying on track. Both revenue and EPS slightly exceeded expectations in the quarter, based on a same-store sales beat. 2024 guidance was reiterated from the previous time Texas Roadhouse provided an outlook. This outlook specifically called for positive same-store sales next year. The stock is flat after reporting and currently trades at $135 per share.

Texas Roadhouse may have had a good quarter, but does that mean you should invest right now? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.