(Bloomberg) — The wave of money making its way into the credit market is acting as a shield for investors against every negative scenario – even the prospect of ever-fewer central bank cuts this year.

Most Read from Bloomberg

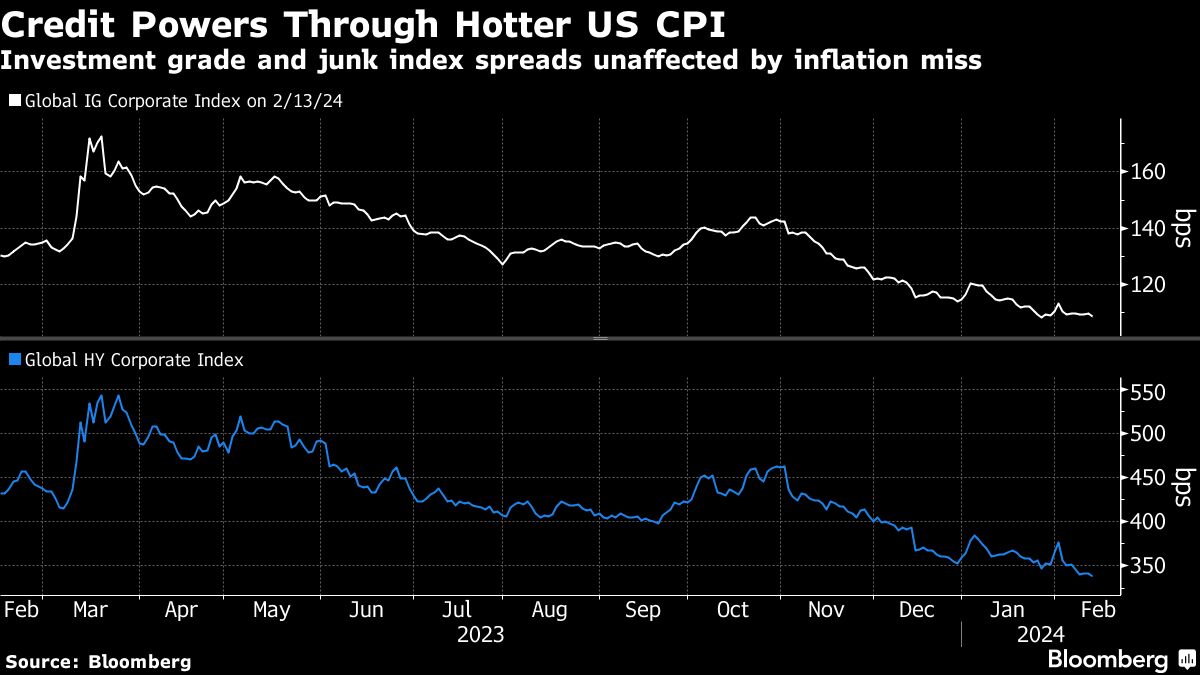

Risk premiums on high-grade and junk bonds fell Tuesday despite hotter-than-expected US consumer-price rises and pushed prospects for the Federal Reserve’s first rate cut firmly into the summer. A gauge of default insurance only rose to levels recorded on Monday.

The continued strength of corporate-bond spreads underscores the numbing effect of persistent flows pouring into credit funds, making managers flush with cash that needs to be invested. Even a blow to the main driver of bullish expectations for bond returns this year — interest-rate cuts by central banks as the battle against inflation approaches its end — is not enough to dent it.

“The overriding driver for the US and European credit markets has been big fund inflows,” said Annabel Rudebeck, head of non-US credit at Western Asset Management. They are likely to continue because “allocations across our different types of client bases are still quite light in government bonds and indeed also corporate bonds.”

Money flowing into funds focusing on high-grade bonds in the US “strengthened considerably” to about $6 billion in the week to Feb. 7, BofA Securities strategists wrote in a note, citing EPFR Global data. In Europe, high-grade funds recorded their 14th weekly inflow in a row and biggest since June 2020, according to BofA.

This has made credit spreads look invulnerable to risks. The extra yield on global investment-grade bonds over similar government bonds dropped by a basis point on Tuesday and hovers near its lowest level in two years, based on Bloomberg indexes. A junk-bond spreads tracker fell to its lowest since January 2022, before central banks started raising rates to tackle runaway inflation.

Credit Spreads

While credit spreads have tightened, yields have moved higher since the start of the year as underlying government bonds have been hit by fizzling expectations of several rate cuts this year. Rates traders started 2024 pricing in more than six 25-basis-point cuts by the Fed and the European Central Bank, based on data compiled by Bloomberg. This has now fallen to closer to four for both.

“Regardless of those expectations being repriced, overall credit is rock solid,” said Andrea Seminara, chief executive officer at Redhedge Asset Management. “Cash inflows are still strong and support is driven by absolute yield buyers,” he said.

To be sure, the relentless spread tightening has made some managers uncomfortable. Gabriele Foa, a portfolio manager at Algebris Investments, said “it’s a good time to lighten up and wait a bit,” as the market is implying a perfect scenario for economic growth, credit risk and interest rates. Foa is among those using credit-default swap indexes as a hedge.

Read more: Traders Are Using Credit Default Swaps to Hedge Rate-Cut Bet

CPI Print

Even with fewer cuts on the agenda, company bonds are in a position where the upcoming fall in yields will boost their performance and lure more investors away from the safer assets to which they resorted when rising rates pummeled fixed income.

The latest US CPI print is “slightly delaying rate cuts probably but I don’t see it as a game changer for credit,” said Elisa Belgacem, senior credit strategist at Generali Investments. And the cuts to come from the Fed and the ECB “will support demand as people will continue to move out of cash and into credit.”

Most Read from Bloomberg Businessweek

©2024 Bloomberg L.P.