Ride-hailing outfit Uber Technologies (NYSE: UBER) has done it again: The company just reported another strong quarter of top and bottom-line growth for the fourth quarter of 2023. It’s increasingly difficult to argue this industry pioneer’s business model isn’t viable.

But fiscal viability isn’t the same thing as being investment-worthy. Is this stock actually worth owning? For risk-tolerant investors who can stomach above-average volatility, Uber stock is worth buying, even after its recent ascent to record highs. Here are four reasons why.

1. Contracted mobility is the future

At its foundation, Uber Technologies helps people get from point A to point B. In many ways, it’s comparable to a taxi service.

Its business model has been so disruptive, however, because its platform connects passengers with drivers using their own vehicles. Without owning a massive fleet of taxis, Uber was able to provide 2.6 billion rides to its customers last quarter.

This business model is proving efficient and beneficial for everyone involved. And yet, this only scratches the surface of the company’s potential. Uber has expanded its ecosystem so contracted drivers are now also delivering food and other items.

Long-term outlooks for the ride-hailing industry range from Mordor Intelligence’s relatively low expectation of about 9% annual growth through 2029 to Coherent Market Insight’s more bullish estimate of 19% growth through 2030.

Even at the low end of this range, that’s growth worth plugging into.

2. Superior technology makes it easy for consumers and drivers

At the heart of Uber’s business is its mobile app, which remotely connects millions of drivers with tens of millions of riders every single day. This is no small task.

The company has invested billions of dollars in research and development in recent years to refine the app and the technology behind it. It’s still making these investments too, dishing out $784 million in R&D spending last quarter.

Uber’s investment in its technology is well worth it, however. A smooth, reliable user experience is necessary when there’s little to no brand loyalty in the industry. Both riders and drivers can quickly cycle between competing platforms in search of the best rates or shortest wait times. An app that creates as little friction as possible is a powerful competitive advantage in this space.

3. The business model favors one dominant name

The competitive dynamics in some industries support the existence of different brands and service providers because customers demand choice. But other kinds of businesses tend to prop up one dominant name.

Compare the automobile and social media industries, for instance. Consumers want a wide range of choices when shopping for a vehicle, allowing a large variety of major automakers to coexist. However, network effects make social media a completely different kind of enterprise. Meta Platforms‘ Facebook is the dominant name in the space, with a two-thirds share of the social media market, according to GlobalStats. Because it’s by far the largest platform, it’s naturally the default option for many users to establish their online persona.

The ride-hailing industry is in many ways comparable to the social media business — the more users on a platform, the more valuable it becomes. This goes for both riders and drivers, and it explains how Uber has been able to win control of 75% of the U.S. ride-hailing market, according to numbers compiled by Bloomberg.

For years, Uber was plagued by steep losses in its fight for market share, but that scale is now paying off for the company.

4. Growth, growth, and more growth

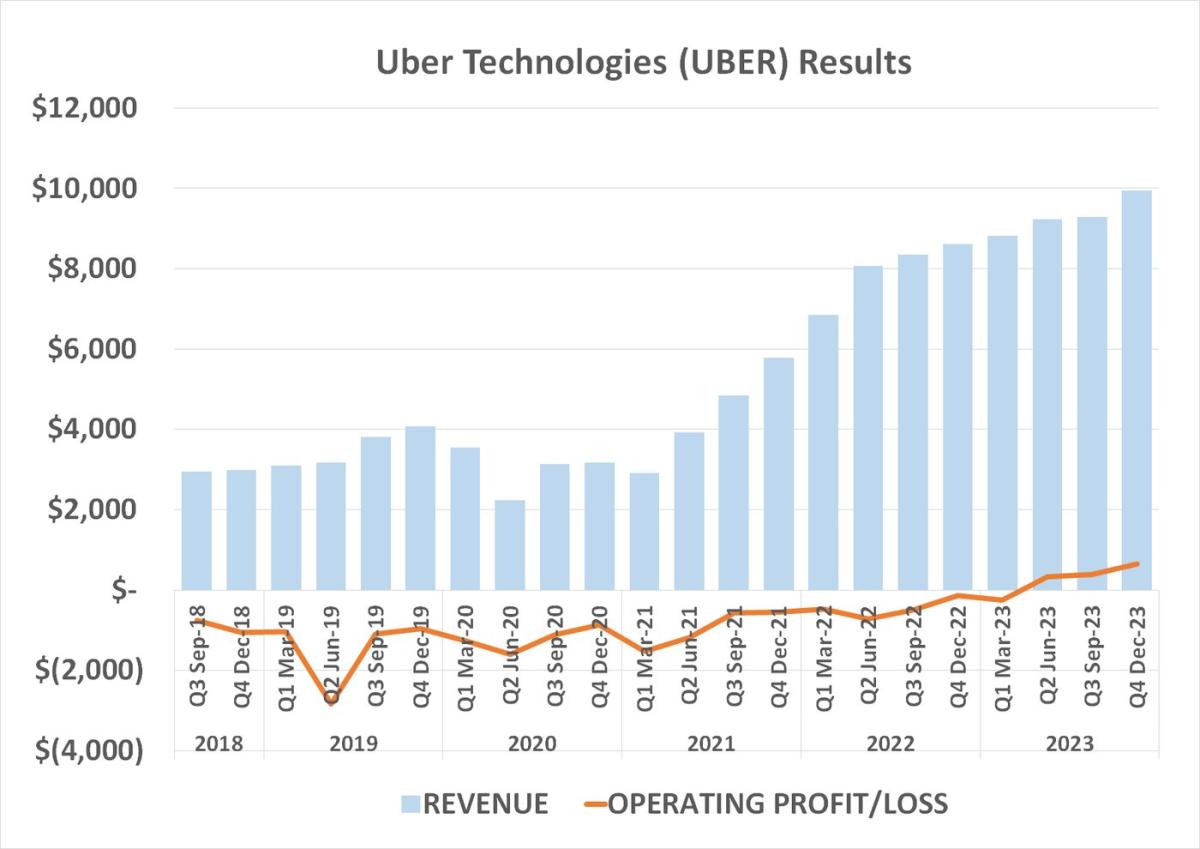

You only have to look at Uber’s most recent results to see business is good for the industry leader. While Factset reports that S&P 500 companies are expected to report fourth-quarter revenue growth of just 3.5%, Uber saw bookings in that quarter grow 21% on a currency-adjusted basis. Its net income, cash flow, and earnings before interest, taxes, depreciation, and amortization (EBITDA) also soared in Q4, outperforming the 1.6% earnings growth expected for the S&P 500.

The thing is, Uber’s fourth-quarter numbers are anything but an outlier. Better yet, its top-line growth continues to help widen the company’s profitability, which first materialized during the last quarter of 2022.

Analysts are looking for 2023’s full-year top line of $37.3 billion to swell to nearly $70 billion by 2028, while its per-share earnings of $0.87 could more than double to $2.08 as soon as 2025. That’s huge on both fronts.

Should you invest $1,000 in Uber Technologies right now?

Before you buy stock in Uber Technologies, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Uber Technologies wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of February 5, 2024

Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool’s board of directors. James Brumley has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Meta Platforms and Uber Technologies. The Motley Fool has a disclosure policy.

4 Reasons to Buy Uber Stock Like There’s No Tomorrow was originally published by The Motley Fool