When the COVID-19 pandemic began in March 2020, Peloton Interactive (NASDAQ: PTON) stock was trading at around $25 per share. By the end of that year, it soared to over $150 as demand for the company’s at-home exercise equipment exploded.

Today, Peloton stock is down more than 97% from that peak, and it trades near its all-time low of about $4. Since society is now free from the pandemic-era restrictions that shut down gyms and limited outdoor activities, demand for Peloton’s products has plunged.

The company installed a new CEO, Barry McCarthy, in early 2022 to right the ship, but the progress hasn’t impressed investors. Three things continue to drive the decline in Peloton stock, and the worst is far from over.

1. Peloton’s revenue is shrinking

People raced to get their hands on Peloton’s equipment — which now includes a stationary exercise bike, treadmill, and rowing machine — during the pandemic lockdowns so they could work out at home. All of Peloton’s flagship products feature a digital screen so users can stream virtual fitness classes, as well as music and entertainment, at their discretion.

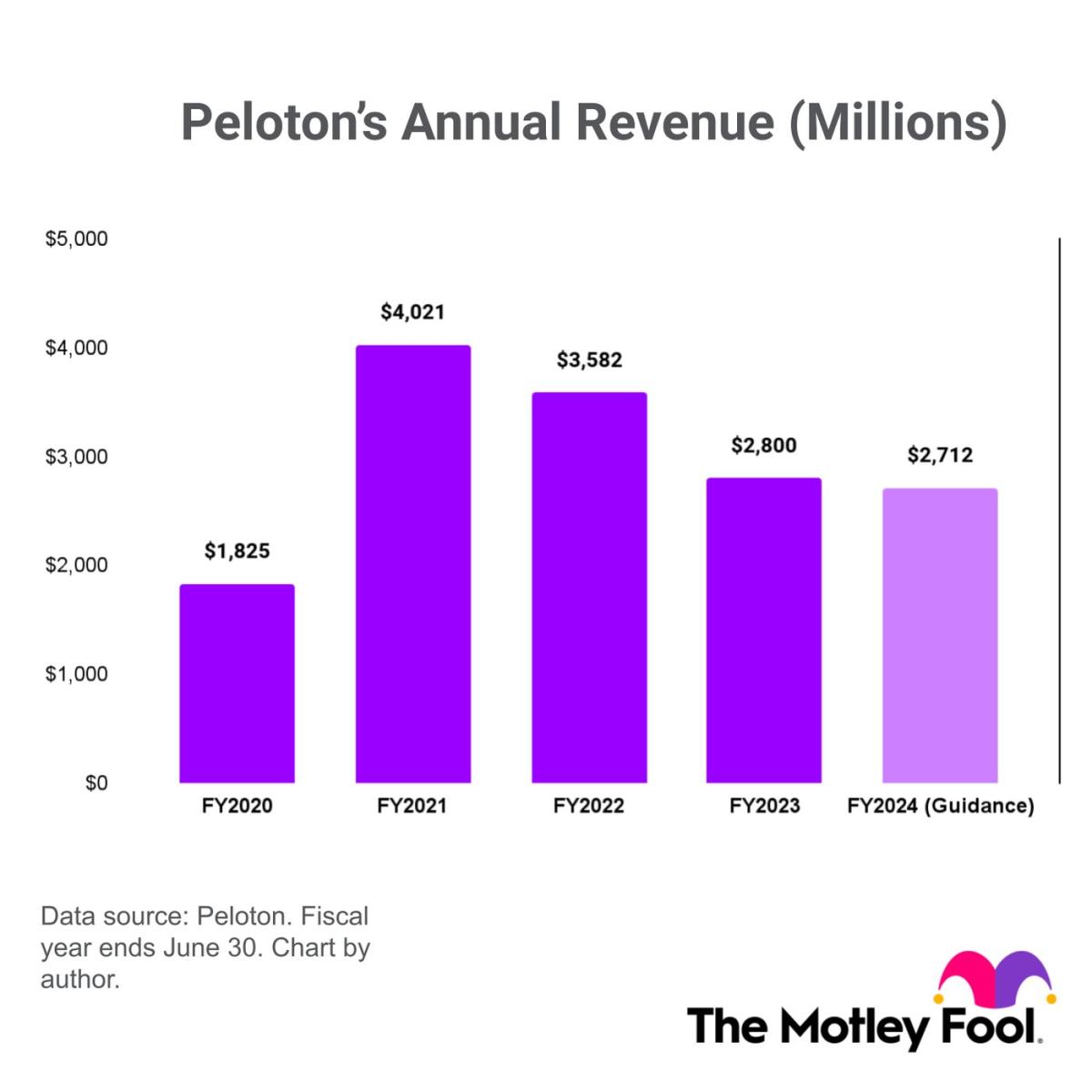

Peloton was the brand of choice for many fitness enthusiasts grappling with social restrictions. As a result, the company’s revenue more than doubled from the previous year to $4 billion in fiscal 2021 (ended June 30, 2021).

But that turned out to be the peak. The company hasn’t found a way to reverse its evaporating demand, despite McCarthy’s best efforts. He cut deals with third-party retailers like Amazon and Dick’s Sporting Goods to sell Peloton’s equipment outside of its own sales channels for the first time. He even introduced a rental program so customers could own a Peloton on a subscription basis, without forking over thousands of dollars upfront. So far, those initiatives haven’t reignited Peloton’s revenue growth.

Peloton’s revenue sank in fiscal 2022 and fiscal 2023. In the recent fiscal 2024 second quarter (ended Dec. 31, 2023), revenue shrank yet again, and management’s forecast for the full year now points to another annual decline.

2. Peloton is generating persistent financial losses

One of McCarthy’s greatest challenges was to stem Peloton’s spiraling losses. The previous management team expected sales to continue growing after the blockbuster result in fiscal 2021, so they more than doubled the company’s operating expenses to $3.4 billion in fiscal 2022. They ramped up marketing spending, expanded the workforce, and increased product inventory.

Those ill-fated initiatives combined falling revenue with surging expenses to generate blowout losses. Peloton reported a whopping $2.8 billion net loss that year.

McCarthy has slashed costs since joining the company. He cut Peloton’s workforce by more than half, and he outsourced and offshored its equipment manufacturing. He is even trying to grow Peloton’s digital business with a new health and fitness app designed for new customers who don’t own any of the company’s equipment.

Subscription-based digital apps tend to carry a high profit margin, which could (in theory) offset some of the company’s losses. But Peloton’s app hasn’t even surpassed 1 million sign-ups yet, and it lost members in the most recent quarter.

Peloton generated a net loss of $195 million in its fiscal Q2, and while that improved from a loss of $335 million in the year-ago period, there is still a long way to go. Plus, even after making adjustments to exclude one-off and non-cash expenses like stock-based compensation, Peloton still had negative adjusted EBITDA (earnings before interest, tax, depreciation, and amortization) of $82 million.

3. Peloton’s cash balance is dwindling

When a business has shrinking revenues and persistent losses, it needs a large cash balance to have breathing room to address those challenges. Peloton’s balance sheet could certainly be in better shape.

It has just $738 million in cash on hand, down from $871 million in the year-ago period. It’s also carrying a $691 million loan which it acquired in 2022 just so it could continue to operate.

To be clear, Peloton doesn’t face an immediate risk of running out of money. However, its modest cash balance will restrict the company’s ability to invest in new products or expand its marketing initiatives. In fact, it will be difficult for management take any risks at all because mistakes will be especially costly in this situation. Peloton is unlikely to attract further debt funding, and conducting a capital raise at its current stock price would significantly dilute existing investors.

That means reigniting sales growth won’t be easy from here, which could force management to cut costs even further to prevent steeper losses. That, in turn, could deal another blow to sales.

Escaping this spiral will be an incredible challenge, so the 97% decline in Peloton stock certainly doesn’t make it a buy in my book.

Should you invest $1,000 in Peloton Interactive right now?

Before you buy stock in Peloton Interactive, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Peloton Interactive wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of February 5, 2024

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Anthony Di Pizio has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Amazon and Peloton Interactive. The Motley Fool has a disclosure policy.

3 Reasons This Once Unstoppable Stock Has Plunged 97% was originally published by The Motley Fool