(Bloomberg) — Asian stocks edged lower with the latest data from China underscoring the economy’s weakness. Japanese bond yields pushed higher with the yen following hawkish signals from a summary of the Bank of Japan’s latest meeting.

Most Read from Bloomberg

Key benchmarks in Hong Kong and mainland China posted modest declines, with another month of contraction in factory activity offset by a jump in battery giant Contemporary Amperex Technology Co.’s earnings. The region’s equities were range-bound following disappointing earnings from key US technology companies Microsoft Corp. and Alphabet Inc. ahead of the Federal Reserve’s policy meeting. US equity futures fell.

BOJ board members continued to discuss prospects for ending the negative rate policy during their meeting last week, with a member indicating conditions conditions offer a “golden opportunity.” An increase in rates would be the nation’s first since 2007 and would bring an end to the world’s last negative rate.

“Markets have a lot to chew on today after big tech earnings, while not absolutely disappointing, failed to appease market expectations and could hurt the broader risk sentiment,” said said Charu Chanana, head of FX Strategy for Saxo Capital Markets Pte. “China PMI’s also had little to cheer about, while BOJ hawkish hints are seen to be picking up. FOMC comes next and markets will be scouring for dovish hints.”

The dollar consolidated after retreating in the previous three sessions. Treasury two-year yields and ten-year yields were steady in Asian trading.

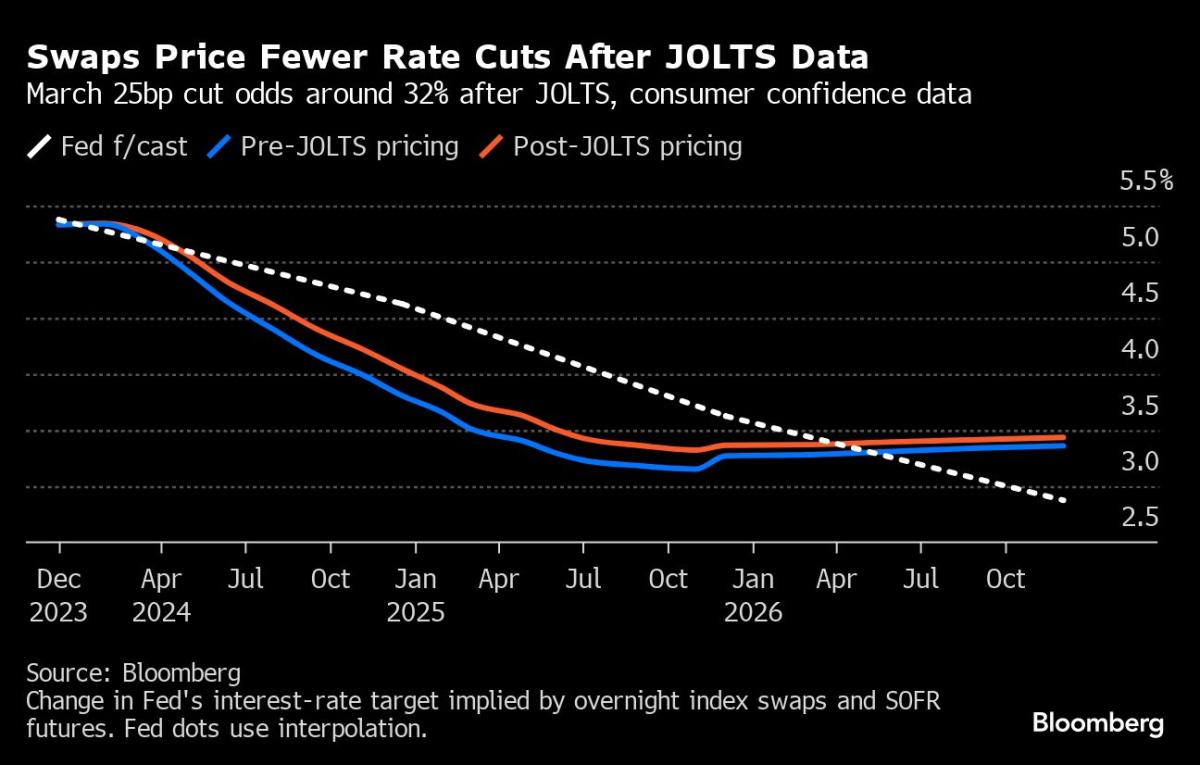

US benchmarks struggled for solid footing in Tuesday’s session as Wall Street digested a hotter-than-estimated reading on job openings, which left investors guessing what Federal Reserve Chair Jerome Powell will say at a rate policy meeting Wednesday. The market further trimmed bets on a March Fed cut.

The Australian dollar and bond fell Wednesday after the country’s headline inflation cooled further in the final three months of 2023, bolstering the case for the Reserve Bank to keep interest rates unchanged next week.

In earnings, Samsung Electronics Co. posted its fourth straight quarter of profit decline in the holiday quarter, after a long-awaited recovery in chip and electronics demand delivered few returns. CATL posted a jump in full-year earnings, allaying investor concerns that profitability could be waning. Alphabet Inc. sank after reporting revenue from its core search advertising business that fell short of estimates and Microsoft’s cloud growth disappointed some on Wall Street.

Resilient market

Swap contracts referencing the March Fed meeting date — the next one after this week’s — now show about a third of a 25-basis-point drop. Late last year, a quarter-point cut in March was completely priced in, reflecting expectations for labor-market cooling that have failed to materialize.

US job openings unexpectedly rose in December to the highest level in three months while fewer Americans quit their jobs. Tuesday’s data kicks off a slew of releases that will offer insights into the state of the labor market. A report due Wednesday is forecast to point to easing employment costs at the end of 2023, while the government’s jobs report Friday is projected to show US employers added around 185,000 positions in January.

“Traders are on edge, anticipating a potential pivot point in the investment market,” said Hebe Chen, an analyst at IG Markets based in Melbourne. “Last night’s job and housing data appear to support a hawkish Fed, casting a shadow on optimism for any near-term easing. Furthermore, the price action following Microsoft and Alphabet’s earnings suggests that the bar to sustain the price rally is now considerably high.”

Elsewhere, oil headed for its first monthly gain since September as an escalation of attacks on ships in the Red Sea spurred a diversion of tanker traffic and raised fears about a wider conflict in the Middle East.

Key events this week:

-

Boeing announces earnings amid US government safety probe, Wednesday

-

Federal Reserve interest rate decision and Fed Chair Jerome Powell’s news conference, Wednesday.

-

US Treasury quarterly refunding, Wednesday.

-

China Caixin manufacturing PMI, Thursday

-

Eurozone S&P Global Manufacturing PMI, CPI, unemployment, Thursday

-

US productivity, construction spending, ISM Manufacturing, initial jobless claims, Thursday

-

Apple, Amazon, Meta, Deutsche Bank, BNP Paribas earnings, Thursday

-

Bank of England interest rate decision, Thursday

-

US employment report, University of Michigan consumer sentiment, factory orders, Friday

Some of the main moves in markets:

Stocks

-

S&P 500 futures fell 0.4% as of 10:23 a.m. Tokyo time

-

Japan’s Topix fell 0.2%

-

Australia’s S&P/ASX 200 rose 0.1%

-

Hong Kong’s Hang Seng fell 0.3%

-

The Shanghai Composite fell 1.8%

-

Euro Stoxx 50 futures fell 0.1%

-

Nasdaq 100 futures fell 0.8%

Currencies

-

The Bloomberg Dollar Spot Index was little changed

-

The euro was little changed at $1.0841

-

The Japanese yen was little changed at 147.49 per dollar

-

The offshore yuan was little changed at 7.1885 per dollar

-

The Australian dollar fell 0.3% to $0.6580

Cryptocurrencies

-

Bitcoin fell 1.6% to $42,828.78

-

Ether fell 1.9% to $2,335.45

Bonds

-

The yield on 10-year Treasuries was little changed at 4.03%

-

Japan’s 10-year yield advanced four basis points to 0.745%

-

Australia’s 10-year yield declined seven basis points to 4.07%

Commodities

This story was produced with the assistance of Bloomberg Automation.

Most Read from Bloomberg Businessweek

©2024 Bloomberg L.P.