Well, it happened. The S&P 500 hit a record high in Friday’s trading, finishing the session at 4,839, and a 2% year-to-date gain for 2024 so far. The index is in a true bull market, and is up 35% since its low point on October 22 of last year. The market rally has been powered by tech stocks and AI, but those are far from the only sectors showing strength.

We can find some of those other sectors using the Smart Score tool, from TipRanks. The Smart Score uses AI tech to sort through the mountain of data generated by the daily activity of the stock market, a mountain that only grows taller in a bull run. The algorithm collates and sorts the accumulated stock data, and compares each stock’s statistics to set of factors that have proven to line up with future outperformance. Every stock is given a score, on a simple scale of 1 to 10, letting investors know at a glance how the shares are likely to move in the short- to mid-term. A look through the Smart Score picks points toward some of the stocks that have opportunity brewing in the current market.

We’ve gotten that process started, and found two Perfect 10s that are also getting top ratings from the Street’s analysts. Let’s dive in.

Boot Barn Holdings (BOOT)

The first Perfect 10 we’ll examine is a retail stock, Boot Barn, in the Western lifestyle niche. The company sells a wide variety of Western-themed gear, including footwear, apparel, and accessories. Specific categories include high-end boots and cold-weather outerwear. The company markets its products through a selection of work and lifestyle brands.

Boot Barn operates through a network of brick-and-mortar stores, as well as its eponymous e-commerce channel. As of November 2 last year, the company’s physical retail network comprised 374 stores across 44 states, giving Boot Barn a nationwide footprint. The company is continuing to expand its network and opened 10 new stores during its last fiscal quarter.

That fiscal quarter covered Q2 of fiscal year 2024 and exhibited mixed results. Boot Barn’s total revenue reached $374.5 million, representing a 6.5% increase from the prior-year quarter, though it fell short of the forecast by $3.08 million. The retailer’s earnings followed the opposite trend; the 91-cent non-GAAP EPS decreased from $1.06 per share in fiscal 2Q22 but exceeded expectations by 2 cents per share.

The increase in earnings occurred despite a 3.8% year-on-year decline in the company’s consolidated same-store sales. This decrease includes a 2.8% drop in retail store same-store sales and an 11.3% drop in e-commerce same-store sales.

Boot Barn’s stock price started 2024 with a 6% dip. But according to UBS analyst Jay Sole, this might be a great opportunity for investors to invest in a sound retailer – one that is expanding its floor space and possesses ample room for income growth.

“BOOT looks well positioned to continue growing as the leading retailer in the western and workwear segments in the US. We anticipate higher store revenues due to positive low- to mid-single-digit comp sales and a ~12.5% annual increase in retail square footage. We expect operating margins to slightly decline due to a structurally higher SG&A structure. Our 5-yr. EPS algorithm includes ~8% annual sales growth and ~5 bps operating margin contraction,” Sole opined.

For Sole, Boot’s shares have earned a Buy rating; his price target, set at $108, implies a one-year upside potential of 50% for the stock. (To watch Sole’s track record, click here)

The UBS view is far from the only bullish take on Boot Barn. The stock has picked up 13 reviews from Wall Street’s analysts, and these include 11 Buys to 2 Holds for a Strong Buy consensus rating. The shares are trading for $71.89 and their $95.08 average target price suggests the stock will gain 32% in the next 12 months. (See BOOT stock forecast)

Teekay Tankers (TNK)

Next on our list is another mid-cap stock, but from a very different sector. Teekay Tankers is an important player when it comes to global oceanic trade, owning and operating a fleet of 52 tanker vessels. These vessels are mainly in the Aframax and Suezmax size ranges, but Teekay also operates 10 LR2 tankers and one VLCC. The company has an international reputation for reliably and safely moving oil from the points of production to where it needs to go.

Teekay is based out of Bermuda, and it operates its fleet through in-house ownership. The size and quality of the company’s fleet – most of the vessels are 10 years old or less – give Teekay a solid base for flexible operations.

Those operations generated $285.86 million in total revenues during the last reported quarter, 3Q23. Teekay’s quarterly revenue was up a modest 2.3% year-over-year and beat the forecast by an impressive $122.83 million. At the bottom line, Teekay realized earnings of $2.24 per share, by non-GAAP measures. This beat the estimates by 14 cents per share; the high earnings reflected the strongest 3Q spot rates for tankers in the past 15 years.

Current events, specifically Middle East tensions and trade disruptions in the Red Sea, have impacted Teekay, providing both tailwinds and headwinds for this oil tanker company. The tailwind comes from higher crude prices, which can boost profits across related industries, while the headwinds are coming from increases in voyage lengths, fuel consumption, and maritime insurance rates.

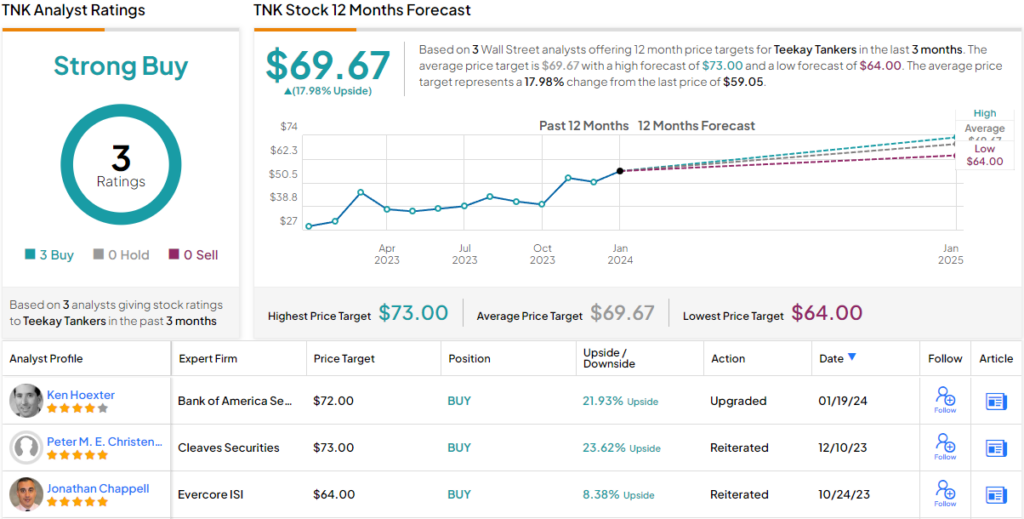

Covering this stock for Bank of America, analyst Ken Hoexter bases his upbeat outlook on the company’s potential upside in light of strong spot rates and longer charter times due to longer voyages.

“Given its elevated spot exposure, Teekay Tankers is highly leveraged to rates, which are likely to see upside following Red Sea disruption and longer haul voyages around the Cape of Good Hope. It remains mostly focused on the spot market (96% of its fleet), having ended most contracts, and on deleveraging its balance sheet, now net cash. We see benefit in deleveraging and longer hauls and upside in rates outpacing the demand decline, supporting our Buy rating on its shares,” Hoexter wrote.

Hoexter goes on to give TNK shares a Buy rating, and a price target of $72 that points toward a 12-month upside potential of 21%. (To watch Hoexter’s track record, click here)

All in all, Teekay boasts a Strong Buy consensus rating, based on 3 unanimously positive recent analyst reviews. The stock is trading for $59.05 and the average target price, at $69.67, suggests a one-year gain of 17%. (See TNK stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.