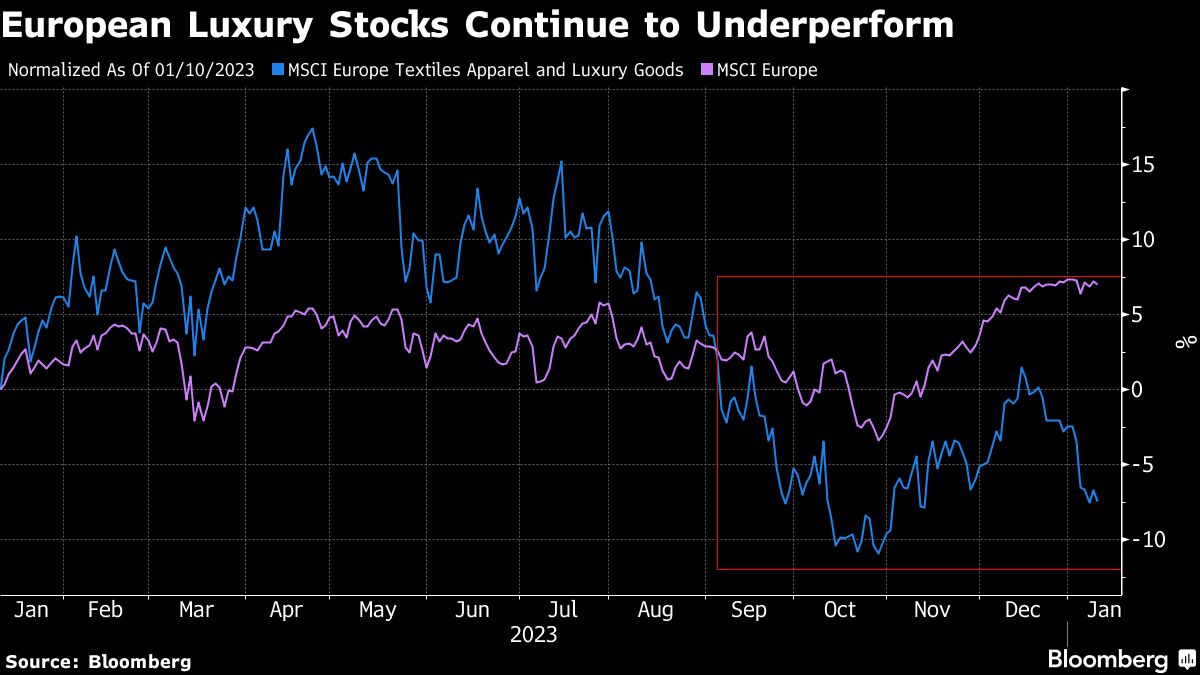

(Bloomberg) — Burberry Group Plc gave Europe’s luxury sector a jolt on Friday with an unexpected profit warning, casting a cloud over peer Cie Financiere Richemont SA, due to report this week.

Most Read from Bloomberg

A shopper slowdown and darkening Chinese economy leaves little room for margin expansion for luxury companies this year, according to analysts at Barclays. Burberry’s revamp may now prove ill-timed, Bloomberg Intelligence’s Deborah Aitken said.

Richemont may paint a slightly healthier picture, although its update may be overshadowed by the company’s failure to offload its stake in the unprofitable online Yoox Net-a-Porter business.

Inventory management will be key if luxury companies are to avoid discounting in the first half, according to BI’s Aitken.

Reports from food delivery companies Just Eat Takeaway.com NV and Deliveroo Plc and online grocer Ocado Group Plc will be scoured for signs of improved profitability as they navigate fickle customer loyalty and shoppers’ return to physical stores, BI said.

Credit bureau Experian Plc and gambling giant Flutter Entertainment Plc are also due.

Highlights to look out for:

Monday: No major results of note

Tuesday: Ocado (OCDO LN) is expected to post a 7.6% jump in fourth-quarter retail revenue, consensus shows. Growth on that front has been picking up pace after the post-pandemic dip, with greater participation from Marks & Spencer products adding heft over the Christmas period, said BI’s Charles Allen. The new Luton unit should spur on efficiency gains, although fully utilized van and driver capacity over the holiday period may have restrained capacity during its peak weeks. Affirmation of its profit target would signal low-double digit Ebitda growth in the second half, Allen said.

-

Experian (EXPN LN) should report “solid” third-quarter results, judging by its confident body language in November, Citi analysts said. Still, challenges lurk as the peak of the interest rates hike cycle puts a lid on credit flows. The credit bureau is well positioned to deliver revenue above consensus in 2024, thanks to diversification in Latin America and a strong North American business that’s not as exposed to mortgage originations as peers, according to BI’s Nathan Dean.

Wednesday: Just Eat Takeaway’s (TKWY NA) fourth-quarter update will reveal just how close orders have come to returning to growth, especially in the UK and Ireland. While consensus points to a 5.7% drop to 226 million overall, the pace of decline in the British Isles likely slowed to 1.1%. Despite reaching cash flow breakeven six months earlier than planned, Just Eat has been weaker than peers on gross transaction volume, and the regulatory situation in the US “remains muddied,” said Morgan Stanley analyst Miriam Josiah. Clarity on US fee caps and who will become the new CFO are also of interest.

Thursday: Richemont’s (CFR SW) constant-currency sales growth in the third quarter may improve sequentially to about 7%, but the underlying trend is slowing, according to BI’s Aitken. Jewelry could deliver high-single-digit percentage gains thanks to its retail mix and less disruption in China than in the year-earlier period. But Swiss-franc strength adds headwinds that could hamper profitability through March, and the sales decline at YNAP probably steepened. The failed sale of Richemont’s stake in the online platform isn’t helping its risk profile either.

-

Flutter’s (FLTR LN) update will set the scene for its US listing on Jan. 29, a step that may better unlock value from its FanDuel business, which is Ebitda profitable “and driving sportsbook structural win margin,” according to BI’s Conroy Gaynor. The nascent US betting market remains a significant opportunity for Flutter, although its bottom line could take a hit unless the final two months of the year yielded a reversal, after the company suffered from bettor-friendly results in the previous quarter.

Friday: Deliveroo’s (ROO LN) fourth-quarter update will be scrutinized for signs that order growth is picking up, as doubts persist over how soon food delivery companies can deliver sustainable profits. Rising volumes and expected margin expansion in 2024 make Deliveroo one of Morgan Stanley’s top picks for the sector, giving it an edge on peers, according to the analysts. If December growth matches or falls short of November, expectations for fourth-quarter gross transaction value in the UK and Ireland may be overly optimistic, Citi analysts caution.

–With assistance from James Cone, April Roach, Paula Doenecke and Henry Ren.

Most Read from Bloomberg Businessweek

©2024 Bloomberg L.P.