Dividend stocks can be an excellent addition to a diversified investment portfolio, providing both income and growth potential. Furthermore, ultra high-yield dividend stocks generate significant regular income, which is especially beneficial for retirees or those looking for consistent cash flow.

While ultra-high yields are appealing, there are additional factors to consider before investing in dividend stocks. Let’s see if these three stocks, which pay ultra-high yields, meet those other criteria.

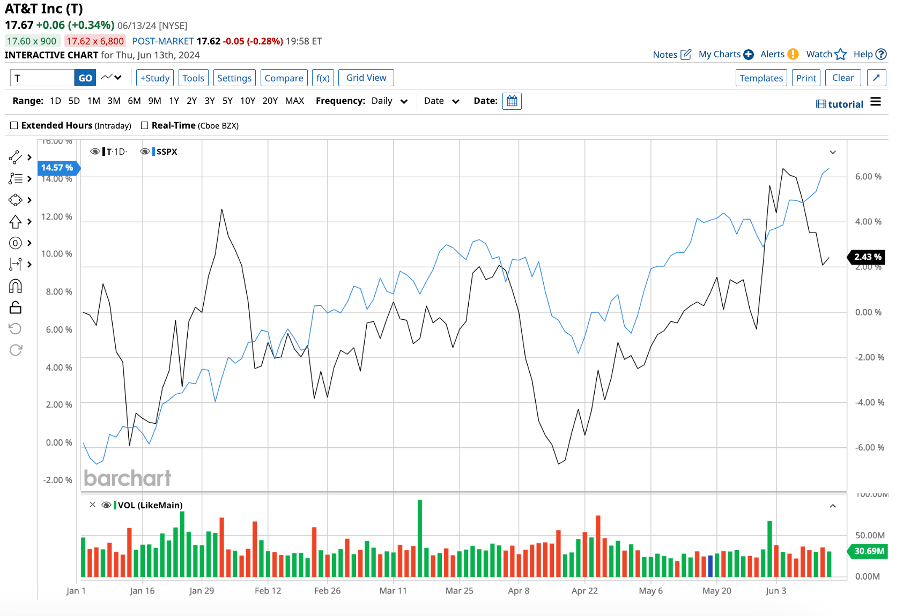

#1. AT&T

AT&T (T) is a telecommunications powerhouse with a rich history dating back to 1983. Over time, it has expanded its offerings to include wireless communications, broadband, and digital entertainment. Its acquisition of Time Warner represented a significant expansion into the media and entertainment sectors.

Valued at $126 billion, AT&T stock is up 5.1% year-to-date, compared to the S&P 500 Index’s ($SPX)gain of 13.8%.

One of the most appealing aspects of AT&T stock to investors has been its dividend yield. AT&T has an annualized forward dividend yield of 6.3%, which is much higher than the communications sector average of 2.6%. Its forward payout ratio of 48.3% indicates that dividends are safe for now, and may increase if earnings continue to rise.

In the most recent quarter, adjusted EPS (earnings per share) of $0.55 came in lower than $0.60 in the year-ago quarter.

The company has struggled with significant debt levels, owing primarily to its aggressive acquisition strategy. Its debt-to-equity ratio of 1.12 is relatively high. The company’s net debt stood at $128.7 billion as of March 31. The company generated $3.1 billion in free cash flow during the quarter, and expects to generate $17 billion to $18 billion for the year.

Generating positive FCF is critical to managing debt levels. The company’s ability to manage debt and generate consistent cash flows will determine whether these dividend payments can be sustained. AT&T expects adjusted EPS to increase in 2025, in line with consensus estimates.

Overall, Wall Street rates T stock a “moderate buy.” Of the 20 analysts covering T, 10 have rated it a “strong buy,” one has a “moderate buy” recommendation, and nine suggest a “hold.”

Based on its mean price target price of $20.65 from analysts, T stock has an upside potential of 17% from current levels. Plus, its high target price of $29 implies the stock could rally as much as 64%.

#2. Pfizer

Pfizer (PFE) is a global pharmaceutical giant known for its broad portfolio of medicines, vaccines, and consumer healthcare products. Pfizer stock offers a combination of stability, growth potential, and dividend income.

Valued at $156.7 billion, Pfizer stock has dipped 4.4% YTD, compared to the broader market.

In the recent first quarter, total revenue dipped 19% to $14.9 billion, due to lower sales of Comirnaty and Paxlovid (used to treat coronavirus). However, excluding these, revenue increased by 11%. Adjusted EPS fell 33% year-over-year to $0.82.

The company paid out $2.4 billion in cash dividends. Pfizer pays an annualized forward dividend yield of 6.08%, higher than the healthcare sector average yield of 1.6%. Its forward payout ratio of 61.6%, while slightly high, indicates that its current earnings can cover dividend payments. The pharma giant has increased dividends for the last 14 years.

Pfizer’s strong product pipeline, along with its strategic focus on high-growth therapeutic areas, presents significant growth opportunities. The company’s Seagen acquisition last year to strengthen its oncology portfolio, and nine new approved products in 2023 could help boost its earnings going forward.

Analysts covering Pfizer stock expect its earnings to increase by 27.3 % in 2024, before further jumping by 16.7% in 2025.

Overall, Wall Street rates Pfizer stock a “moderate buy.” Of the 21 analysts covering PFE, eight have rated it a “strong buy,” one has a “moderate buy” recommendation, and 12 suggest a “hold.”

Based on its mean price target price of $33.37, PFE stock has an upside potential of 21.2% from current levels. Its high target price of $54 implies the stock could rally as much as 96.1%.

#3. Altria

Altria Group (MO) is a leading player in the tobacco industry. It has long been a staple in many income-focused portfolios, due to its high dividend yield.

Valued at $78.5 billion, Altria’s stock is down 9.8% year-to-date.

Altria pays a high annualized forward dividend yield of 8.6%, richer than the consumer sector average yield of 1.9%. It paid out $1.7 billion in dividends in the first quarter.

Its forward payout ratio of 73.9% is on the higher side. With declining cigarette…

Read More: 3 Ultra High-Yield Dividend Stocks to Pounce On at Every Dip