Given the two stocks’ different responses to the release of first-quarter numbers, it would be easy to assume the best for ride-hailing outfit Lyft (NASDAQ: LYFT) while presuming the worst for bigger rival Uber Technologies (NYSE: UBER). Shares of the former soared in response to its Q1 results while Uber stock tanked.

The market may be misreading both sets of quarterly reports, though, and aggravating that mistake by buying Lyft and selling Uber. Uber is actually the better stock to own here, while Lyft arguably isn’t worth owning at all. Here’s the deal.

Expectations are everything — until they aren’t

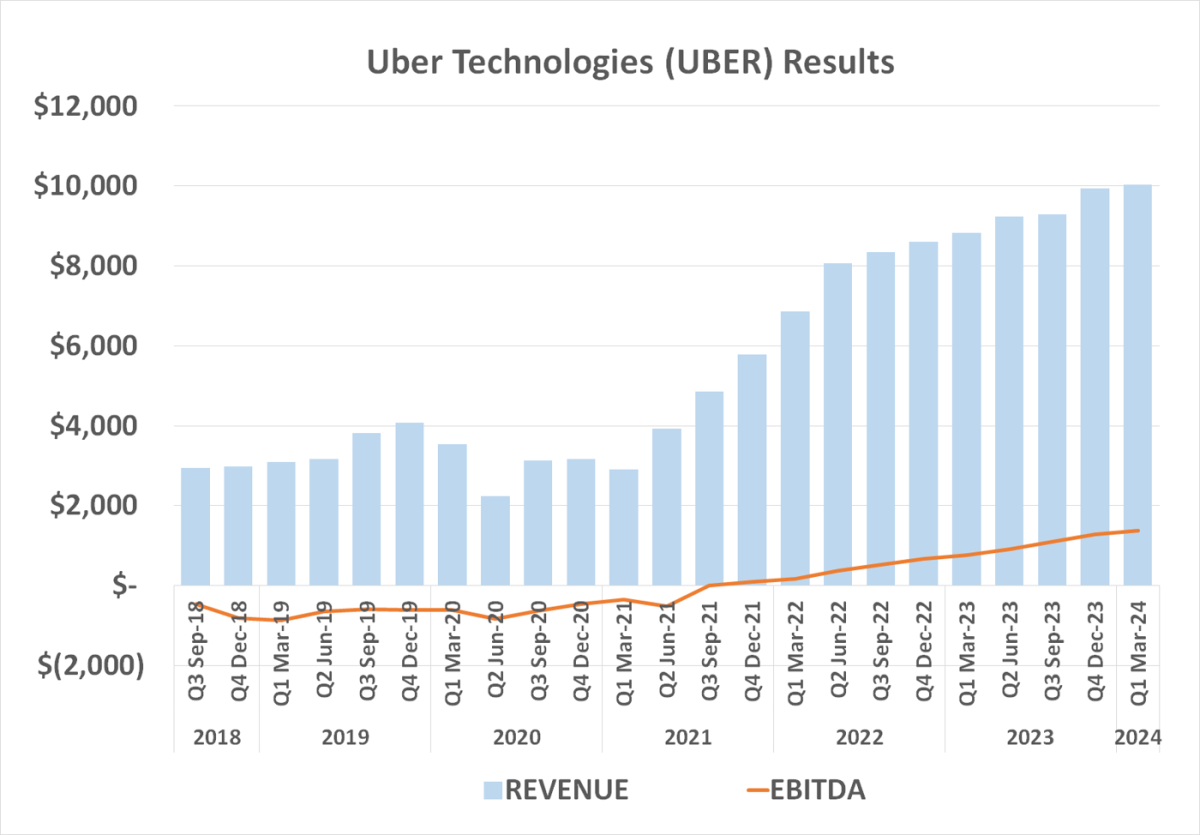

It’s curious to say the least. Uber turned $10.13 billion worth of revenue into operating income of $172 million last quarter, up 15% from its year-earlier top line, and reversing the Q1 2023 operating loss of $262 million. Analysts were only calling for sales of $10.1 billion.

The culprit for the stock’s sell-off? After factoring in a $721 million charge for “unrealized losses related to the revaluation of Uber’s equity investments,” the ride-hailing outfit ultimately reported a GAAP loss of $654 million. The crowd was also fixated on the company’s Q2 booking guidance of between $38.75 billion and $40.25 billion, which came up a little shy of estimates.

Not even the company’s expectation for adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) of between $1.45 billion and $1.53 billion for the quarter now underway — roughly a 60% year-over-year improvement — could sway investors, who dragged the stock nearly 6% lower on Wednesday.

At the other end of the spectrum, Lyft shares jumped more than 7% on Wednesday following Tuesday’s post-close release of its first-quarter results. Adjusted earnings of $0.15 per share on revenue of $1.28 billion were both year-over-year improvements. And both came in better than the $0.06 per-share profit and sales of $1.16 billion analysts were anticipating.

The company’s projected gross bookings (the total passenger fees collected) of between $4 billion and $4.1 billion for Q2 also topped expectations of just under $4 billion. Not bad. There are some important details not readily evident in these basis numbers, however, that tell the rest of the story.

Take a step back and look at the bigger picture

Don’t misunderstand, it would have been nice to have some sort of warning from Uber that it was going to book a sizable accounting charge last quarter. Credit must also be given where it’s due — Lyft’s Q1 revenue growth of 28% is rock-solid to be sure.

But there’s more to the story.

Take Uber’s reported and predicted bookings as an example. Its first-quarter gross bookings were still up 20% year over year, while its outlook for second-quarter bookings implies growth of somewhere between 18% and 23%. This growth pace is in line with Q4’s and quietly sets the stage for an acceleration of last year’s overall gross bookings growth.

There’s also the not-so-minor detail that Uber is considerably more profitable than Lyft is — not just on an absolute basis, but on a relative one as well. Uber’s adjusted Q1 EBITDA of $1.38 billion is 13.6% of the quarter’s total revenue.

Lyft’s comparable EBITDA of $59.4 million may also be well up from year-ago levels, but that’s still a profit margin of less than 5% of its top line for the quarter in question. This is a critical nuance. Should a price war materialize, Uber is in a much better position to wage it.

But is everything relative to a particular stock’s price when it comes to jumping into a new trade? If so (and this is certainly true often enough to consider before stepping into any investment), even then Uber Technologies holds its place as the better pick.

See, Uber stock was already down 14% from March’s peak prior to Wednesday’s plunge, whereas as of Tuesday’s close, Lyft shares were trading at more than twice their price from just a year earlier. They’re now just 5% below their March peak, while Uber shares are trading more than 20% below that comparable high.

This good and bad news already seems to have been priced into each stock, with Wednesday’s movement unnecessarily pricing in investors’ views again.

Uber stock is the better bet of the two

Don’t misread the message. It’s possible for both stocks to make bullish progress from here, just as it’s possible that economic turbulence could work against both stocks. It’s even possible — albeit unlikely — Lyft shares could continue rallying while Uber stock continues to fall. Never say never.

Looking through a level-headed risk-versus-reward lens, however, one of these names is clearly a better bet than the other. That’s Uber. The market was just so distracted by the comparison of each company’s results and guidance to expectations on Wednesday that it lost sight of each outfit’s absolute results. It happens. It’s also a mistake likely to be corrected sooner or later, and probably sooner rather than later.

Should you invest $1,000 in Uber Technologies right now?

Before you buy stock in Uber Technologies, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Uber Technologies wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $550,688!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of May 6, 2024

James Brumley has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Uber Technologies. The Motley Fool has a disclosure policy.

3 Reasons I’ll Take Uber Stock Over Lyft Despite the Lousy Response to Q1 was originally published by The Motley Fool