The share prices of many dividend-paying companies have been under pressure over the past couple of years because of rising interest rates. Higher rates increased their borrowing costs and made lower-risk alternative investments like bonds and bank CDs more attractive, which caused dividend yields to rise to compensate investors for their higher risk profiles.

However, that headwind should fade in 2024. Because of that and some company-specific factors, dividend yields could compress this year as share prices rise.

That makes now the time to buy high-quality, high-yielding dividend stocks before their yields fall from their more attractive levels. Stanley Black & Decker (NYSE: SWK), Enbridge (NYSE: ENB), and Clearway Energy (NYSE: CWEN)(NYSE: CWEN.A) currently stand out to these three Motley Fool contributors as higher-yielding dividend stocks that income-focused investors will want to scoop up before it’s too late.

Stanley Black & Decker’s earnings seem set to rebound in 2024

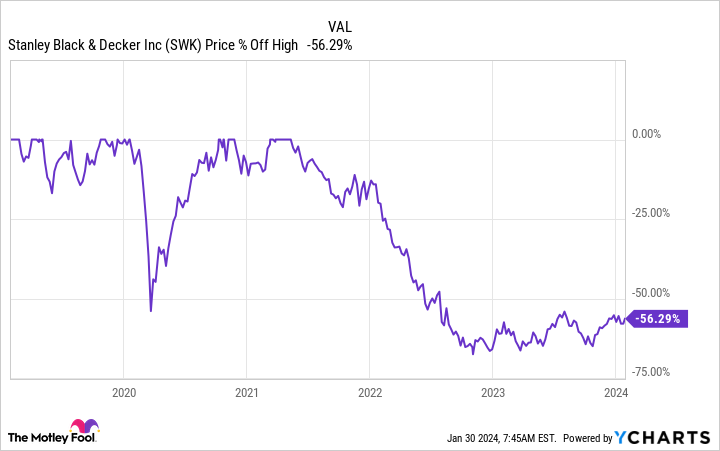

Reuben Gregg Brewer (Stanley Black & Decker): The last couple of years have been really bad for this Dividend King. Adjusted earnings hit a record in 2021 of $10.48 per share. In 2022, Stanley earned less than half of that at $4.62. And in 2023, the industrial company’s downward trend continued, as it reported full-year earnings of $1.45 per share, another drop of more than 50%.

It’s little wonder the stock has fallen so dramatically, with the shares down more than 50% from their 2021 highs. But management has been hard at work streamlining the business, by increasing efficiency, paying down debt, and raising prices, among other things.

Success in its efforts has come in many forms, but one of the most notable is that adjusted gross margins have now increased for four consecutive quarters.

Meanwhile, when Stanley Black & Decker released its fourth-quarter earnings, it provided adjusted earnings guidance for 2024. At this point, management is expecting the figure to fall to between $3.50 and $4.50 per share. After a few bad years on the earnings front, it looks like Stanley could finally be in for a good one.

If the company can actually turn the earnings trend higher again, Wall Street is likely to materially alter its view of the stock. The 3.4% dividend yield offered today remains near historically high levels, but perhaps not for long.

Headwinds should turn into tailwinds

Matt DiLallo (Enbridge): Shares of Enbridge have shed more than 10% of their value over the past year. That has pushed the Canadian infrastructure company’s dividend yield up to 7.5%.

Two factors have weighed on the company: interest rates and a massive acquisition. Higher interest rates have increased the borrowing costs of companies like Enbridge while weighing on the valuations of higher-yielding dividend stocks. On top of that, Enbridge agreed to buy three natural gas utilities from Dominion Energy in a $14 billion transaction. That’s a sizable acquisition, which adds some risk.

These headwinds could turn into tailwinds in 2024. The Federal Reserve has said it will begin cutting interest rates in 2024, which should reduce Enbridge’s borrowing costs while lifting some of the weight off its stock price.

Meanwhile, Enbridge sees the Dominion deal as a once-in-a-generation opportunity to acquire three high-quality natural gas utilities at a historically attractive valuation. That deal will also significantly enhance the company’s cash flow and growth profile.

Besides that deal, Enbridge should continue benefiting from its massive organic growth backlog. After closing the Dominion deals, the company will have over 24 billion Canadian dollars ($17.9 billion) of expansion projects in its backlog.

And it has many more projects under development. Enbridge believes it can grow its earnings about 5% annually over the medium term. That should give it the power to continue pushing its high-yielding payout higher.

Add that growing income stream to the company’s lower share price, and Enbridge could produce high-powered total returns in the coming years as its headwinds fade and growth ramps up.

An attractive buy ahead of earnings

Neha Chamaria (Clearway Energy): After a solid rebound in the last quarter of 2023, shares of Clearway Energy are struggling to maintain momentum and have lost nearly 13% so far this year, as of this writing.

For income investors, this is a great opportunity to buy this renewable energy stock. It offers a high yield of 6.4% and aims to increase its dividend by 7% this year, in line with its long-term target range of 5% to 8% in divided growth through 2026. Even better, Clearway Energy is confident of supporting its dividend growth through cash flows without resorting to debt or stock sales.

Clearway Energy sells power it produces under long-term contracts and therefore generates steady cash flows, which is the primary reason it can afford to pay regular dividends.

The company also has manageable debt and is consistently investing in growth projects to generate higher cash available for distribution (CAFD) and support bigger dividends. Last quarter, for instance, Clearway Energy reiterated its 2023 CAFD guidance of $330 million to $360 million while projecting CAFD of $395 million for 2024. The sale of its thermal business in 2022, in particular, left the company with a lot of cash to deploy into new growth with high CAFD yields.

Since it increases dividends quarterly, you can expect this year’s first dividend raise from the stock in the coming weeks close to the fourth-quarter earnings release on Feb. 22. With the company’s projects and plans already in place to spur dividend growth through 2026, the stock’s recent price drop offers a compelling buying opportunity.

Should you invest $1,000 in Enbridge right now?

Before you buy stock in Enbridge, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Enbridge wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of January 29, 2024

Matthew DiLallo has positions in Clearway Energy and Enbridge. Neha Chamaria has no position in any of the stocks mentioned. Reuben Gregg Brewer has positions in Dominion Energy, Enbridge, and Stanley Black & Decker. The Motley Fool has positions in and recommends Enbridge. The Motley Fool recommends Dominion Energy. The Motley Fool has a disclosure policy.

Don’t Miss Out: 3 High-Yield Stocks to Buy Today was originally published by The Motley Fool