The Nasdaq-100 Technology Sector index has been in scintillating form over the past year, with impressive gains of 53%. Investors have been buying tech stocks hand over fist amid the cooling inflation, a strong economy, and new catalysts such as artificial intelligence (AI) that boosted confidence in this sector.

The good news is that the Nasdaq could continue to head higher in 2024. History suggests that the year in which the Nasdaq clocked gains of 40% or more is usually followed by another year of solid growth. More specifically, the Nasdaq-100 recorded an average gain of 24% in the year that follows a year of 40%-plus increase.

There is a good chance the Nasdaq-100 indeed heads higher in 2024 thanks to several favorable developments: an expected reduction in interest rates, a lowered chance of recession, and a further drop in inflation.

That’s why now would be a good time to buy shares of Alphabet (NASDAQ: GOOG) (NASDAQ: GOOGL) and Datadog (NASDAQ: DDOG), two Nasdaq-100 components that delivered impressive gains in the past year and look set for more upside.

1. Alphabet

Shares of tech giant Alphabet jumped 55% in the past year, and the good part is that investors can still buy this Nasdaq stock at an attractive valuation. Alphabet stock is now trading at 27 times trailing earnings, which is a discount to the Nasdaq-100’s trailing earnings multiple of 30. What’s more, Alphabet’s forward price-to-earnings ratio of 22 points toward a nice jump in its bottom line, and the multiple is lower than the Nasdaq-100’s forward earnings multiple of 28.

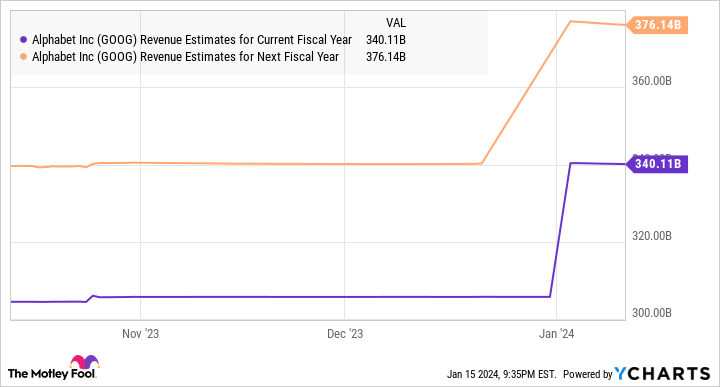

Buying Alphabet at its current valuation looks like a no-brainer considering that its growth is set to accelerate in 2024. Consensus estimates are projecting Alphabet’s 2023 revenue to land at $306 billion, which would be an increase of 8% over 2022. The company is anticipated to show double-digit top-line growth in 2024 and 2025.

A closer look at the prospects of the digital advertising market will make it clear why Alphabet is anticipated to grow at a faster pace this year. According to eMarketer, digital ad spending is predicted to grow 13.2% in 2024, which would be an improvement over the 10.7% growth this market had last year. Given that Alphabet’s Google Search business accounts for nearly 60% of global search advertising revenue, the company is in a solid position to take advantage of the improvement in digital ad spending this year.

More importantly, Alphabet is integrating generative AI tools into its advertising solutions, which should allow the company to consolidate, or even grow, its share in the lucrative digital ad market. The company claims that its AI tools allowed advertisers to increase ad conversions, reduce acquisition costs, and boost subscriber growth by helping them select the right keywords, generate relevant headlines and descriptions, and even select AI-suggested images to improve ad performance.

Alphabet says that advertisers using its AI-powered campaigns witnessed an average of “18% more conversions at a similar cost per action.” Thanks to Alphabet’s AI-powered ad campaigns, the company could gain more share in the search and digital ad market. According to Bloomberg Intelligence, generative AI-driven ad spending could increase from $57 million in 2022 to $64 billion in 2027. By 2032, generative AI-powered ad spending is expected to jump to $192 billion.

Alphabet could keep growing at an impressive pace in the long run thanks to new opportunities such as generative AI. Investors should consider buying this tech stock before it jumps higher.

2. Datadog

Datadog, which is known for providing cloud observability and monitoring solutions, shot up an impressive 74% in the past year. A big chunk of those gains arrived following the company’s third-quarter 2023 results, which were released in November last year.

Datadog shot up big time as the company delivered a strong set of results and raised its full-year outlook. The cloud specialist expects to finish 2023 with $2.1 billion in revenue at the midpoint, which would translate to a 24% jump over 2022 levels. However, don’t be surprised to see Datadog ending 2023 with stronger revenue thanks to an improving customer spending environment and the fast-growing nature of the cloud observability and monitoring market.

According to Datadog’s estimates, its total addressable market (TAM) was worth $45 billion in 2023. So, the company’s 2023 revenue estimate suggests that it hasn’t scratched even 5% of the end-market opportunity it is sitting on. Even better, Datadog expects its TAM to hit $62 billion by 2026 as the growing spending on cloud services will create the need for more observability, monitoring, and security solutions that it provides.

Not surprisingly, Datadog is witnessing healthy growth in its customer base, as well as the fact that its customers are adopting multiple solutions that it sells. For instance, Datadog ended the third quarter of 2023 with nearly 27,000 customers, an increase of almost 21% over the year-ago period. The number of customers who have spent more than $100,000 on its offerings increased 20% year over year.

Bigger customers who generated more than $1 million in annual recurring revenue for the company increased at a much faster pace of 46%. This impressive growth can be attributed to the fact that more customers are adopting multiple Datadog products. For example, 46% of the company’s customers were using four or more of its modules in the third quarter, up from 40% in the year-ago period. The number of customers using more than six Datadog products increased by 5 percentage points during the quarter to 21%.

So, Datadog is pulling the right strings to ensure that it makes the most of the lucrative end-market opportunity on offer. Not surprisingly, analysts are anticipating the company’s bottom line to increase at an annual rate of 33% for the next five years. This could eventually help this cloud stock sustain its impressive rally and head higher, especially considering that the Nasdaq could have another solid year in 2024.

Should you invest $1,000 in Alphabet right now?

Before you buy stock in Alphabet, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Alphabet wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of January 8, 2024

Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Alphabet and Datadog. The Motley Fool has a disclosure policy.

2 Top Growth Stocks to Buy Hand Over Fist Before the Nasdaq Soars Higher in 2024 was originally published by The Motley Fool