Despite the short-term volatility, investors should always keep in mind that investing is a journey best navigated with a long-term mindset. Ideally, you make consistent investments throughout your career to set yourself up to be as financially stress-free as possible in retirement.

With that thought process in mind, I like to add investments to my retirement account that I can passively invest in without worrying too much, which generally leads me to exchange-traded funds (ETFs). Going the ETF route allows you to check many boxes at once, which is why I’m adding the following two to my retirement account in February.

1. Vanguard S&P 500 ETF

If there is one stock I’ll consistently add to my retirement account, regardless of the month, it’s the Vanguard S&P 500 ETF (NYSEMKT: VOO) because it’s as close to a one-stop shop for stocks as you’ll find.

The Vanguard S&P 500 ETF mirrors the S&P 500, which tracks the 500 largest stocks trading on the U.S. market. It has become the primary benchmark for the U.S. stock market and how most companies and funds measure their performance in a given year.

I like to view an investment in an S&P 500 ETF as an investment in the broader U.S. economy because of how much ground it covers and the importance of the companies it includes. The S&P 500 includes companies from all 11 major sectors, but maybe more importantly, it includes virtually all market leaders from these sectors. Below are the included sectors and a notable example from each:

-

Communication services: AT&T

-

Consumer discretionary: Amazon

-

Consumer staples: Procter & Gamble

-

Energy: ExxonMobil

-

Financials: Bank of America

-

Health Care: Johnson & Johnson

-

Industrials: Honeywell

-

Information technology: Apple

-

Materials: Ecolab

-

Real estate: Simon Property Group

-

Utilities: Duke Energy

The Vanguard S&P 500 ETF is also one of the cheapest ETFs on the stock market, with a 0.03% expense ratio ($3 per $10,000 invested). I always stress that even though differences in expense ratios may seem small on paper, they can cost investors thousands of dollars over time. This is especially true when you’re investing for retirement and potentially have decades’ worth of fees.

For perspective, if you were to invest $1,000 monthly and average 10% annual returns over 25 years, you’d have around $1.17 million with a 0.03% expense ratio. If the expense ratio were 0.75% (like Cathie Wood’s popular ARK Innovation ETF, for example), the investment value would drop to around $1.05 million. In this case, a slight 0.72% difference in fees would cost investors roughly $120,000 over that span. Fees matter.

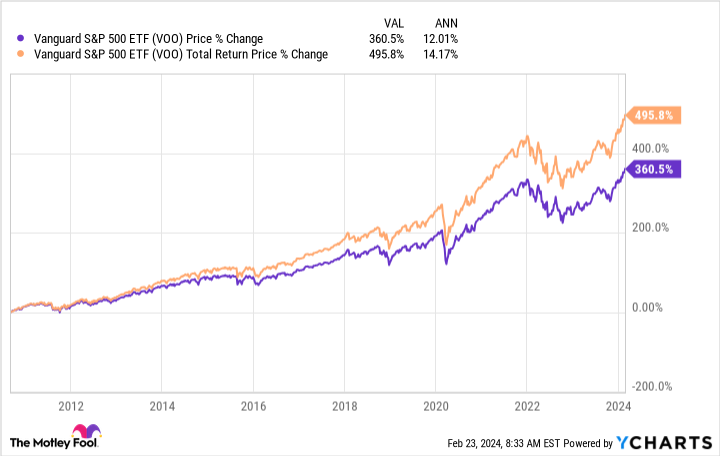

You also can’t go wrong with the Vanguard S&P 500 ETF’s historical results. There’s no way to predict if it will continue at this rate, but it’s a good indication of what’s possible.

2. Schwab U.S. Dividend Equity ETF

The second ETF I’m adding to my retirement account is the Schwab U.S. Dividend Equity ETF (NYSEMKT: SCHD) because of its dividend focus. A lot of attention gets paid to stock price growth (or lack thereof), but dividends can often account for a lot of investors’ total returns. In the past five years, the Schwab U.S. Dividend Equity ETF stock price is up just over 50%. When you include its dividends, its total returns jump to over 78%.

The Schwab U.S. Dividend Equity ETF contains many large-cap stocks you’ll find in the S&P 500, except the focus is on companies that pay above-average and sustainable dividends. It has a dividend yield of around 3.4%, around 2.5 times more than the S&P 500’s current yield. Stock price growth is great, but when investing for retirement, it’s nice to know you have consistent income coming in, regardless of stock price performance.

Using a dividend reinvestment program (DRIP) — which takes the dividends you’re paid and reinvests them into the stock that paid them out — can drastically add to the effects of compound earnings. It’s a way to maximize your total shares until retirement, when you’d ideally begin accepting your dividends in cash payouts.

I think it’s always a good choice to have dividend-focused stocks in a well-rounded retirement portfolio because they can provide an additional income stream in retirement when many people need it most. The Schwab U.S. Dividend Equity ETF can be a good low-cost (0.06% expense ratio) go-to investment.

Should you invest $1,000 in Vanguard S&P 500 ETF right now?

Before you buy stock in Vanguard S&P 500 ETF, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Vanguard S&P 500 ETF wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of February 26, 2024

Bank of America is an advertising partner of The Ascent, a Motley Fool company. John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Stefon Walters has positions in Apple and Vanguard S&P 500 ETF. The Motley Fool has positions in and recommends Amazon, Apple, Bank of America, and Vanguard S&P 500 ETF. The Motley Fool recommends Duke Energy, Ecolab, Johnson & Johnson, and Simon Property Group. The Motley Fool has a disclosure policy.

2 Stocks I Added to My Retirement Account in February was originally published by The Motley Fool