Many quality stocks are overshadowed by high-flying, popular names like Amazon (AMZN), Meta Platforms (META), Nvidia (NVDA), Coca-Cola (KO), and others. Nonetheless, some of these under-the-radar stocks have high growth potential. Investors can potentially earn significant returns by identifying companies with strong fundamentals and growth potential that have yet to be recognized by the broader market. In this article, we’ll look at two such stocks.

Global-E Online (GLBE) offers a comprehensive platform that enables cross-border e-commerce. The broader trend in e-commerce, in which consumers increasingly look beyond their national borders for a variety of products, has increased demand for the Global-E platform, resulting in double-digit revenue growth.

Meanwhile, Snowflake (SNOW) is establishing itself as a strong contender in data management and analytics, with the incorporation of artificial intelligence (AI) into its products.

While Snowflake and Global-E Online are down year-to-date, Wall Street expects these stocks to soar byas much as 25% to 53% over the next 12 months. Both companies are set to report earnings this month, and another strong quarter could drive their stock prices higher. Let’s see if now is a good time to seize these under-appreciated growth opportunities.

Global-E Online Stock

Founded in 2013, Global-E Online (GLBE) provides end-to-end solutions for international e-commerce, simplifying the complex processes involved in selling products across borders.

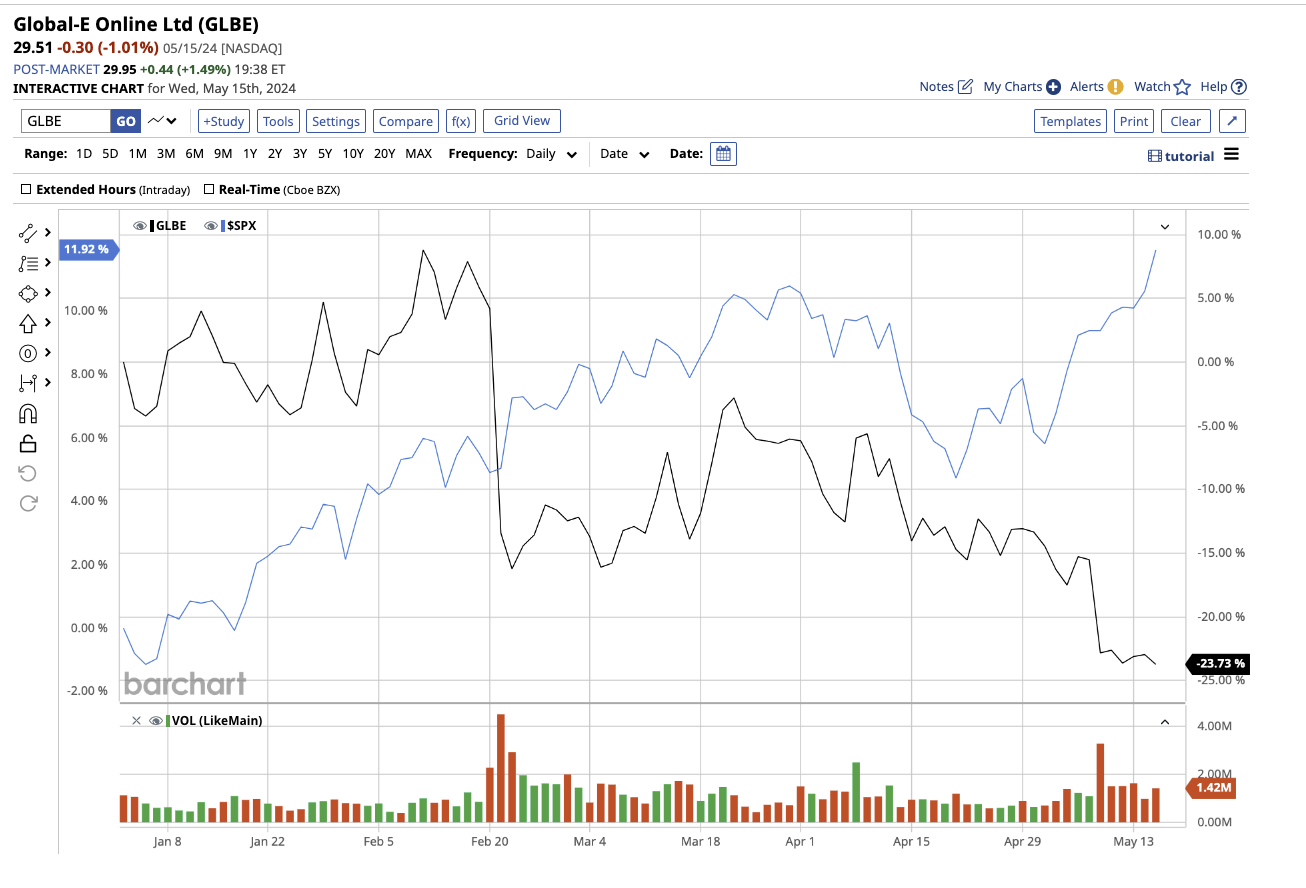

Valued at $4.85 billion, GLBE stock is down 28.6% YTD, compared to the S&P 500 Index’s ($SPX)gain of 11.3%.

The company supports over 200 destinations worldwide, and accepts over 100 currencies. This level of customization is what has attracted customers to its platform, driving its financial performance.

Over the last five years, Global-E’s revenue has grown at a compounded annual growth rate of 54%.

In 2023, Global-E reported a 39.3% year-over-year increase in revenue to $569.9 million, driven by an uptick in the number of merchants using its platform and higher transaction volumes. Gross merchandising volume (GMV) in 2023 touched $3.5 billion, an increase of 45% over 2022.

Though the company reported a net loss of $1.24 per share in 2023, analysts expect Global-E to report a profit of $0.69 per share in 2024, and increase to $0.99 in 2025.

The company will report its first quarter of 2024 results on May 20. Management anticipates Q1 revenue growth of 18% to 23% and adjusted EBITDA to land between $16 million and $20 million.

For the full fiscal year 2024, management forecasts revenue growth of 28% to 35% to a range between $731 million and $771 million. Analysts’ revenue estimates for the year fall within that same range, with 32% growth expected by 2025. Trading at six times forward sales, Global-E makes a compelling case for an undervalued growth opportunity for the long haul.

Following its robust Q4 results, Jefferies analyst Samad Samana reiterated his “buy” rating for the stock with a target price of $45. Samana believes the company will achieve organic GMV growth in the “mid-to-high 30s percentage” in 2024, which is a key indicator of its financial health. The analyst also believes Global-E profits will increase along with sales.

Overall, Wall Street is bullish, rating GLBE stock a “strong buy.” Of the 12 analysts who cover the stock, eight rate it as a “strong buy,” two as a “moderate buy,” and two as a “hold.” The average target price of $43.42 for GLBE indicates a 53% premium over current levels. Furthermore, the stock’s Street-high estimate of $50 implies a potential gain of 76.2% over the next 12 months.

Snowflake Stock

Snowflake (SNOW) offers a cloud-based data platform that enables enterprises to consolidate data into a single, easy-to-use system. The company’s customer base includes a diverse range of industries, from finance and healthcare to retail and technology.

Valued at $54.9 billion, SNOW stock is down 16.7% YTD, compared to the tech-heavy Nasdaq Composite’s ($NASX)gain of 11.3%.

The increasing adoption of its platform by both new and existing customers has contributed to Snowflake’s overall strong performance.

In the fourth quarter of fiscal 2024, Snowflake’s total revenue increased 32% year over year to $774.7 million. Product revenue of $738.1 million made up the majority of the total revenue, with professional services accounting for the remainder.

In Q4, its net revenue retention rate was 131%, indicating that the company is growing rapidly. Plus, Snowflake’s remaining performance obligations (RPO), or contractual revenue that has yet to be recognized, increased by 41% to $5.2 billion.

The company maintained a…

Read More: 2 Stocks Flying Under The Radar That Could Soar This Year