Like bargains? Check out Peloton Interactive (NASDAQ: PTON). Shares of the fitness equipment and related tech company are down an incredible 97% from their early 2021 peak.

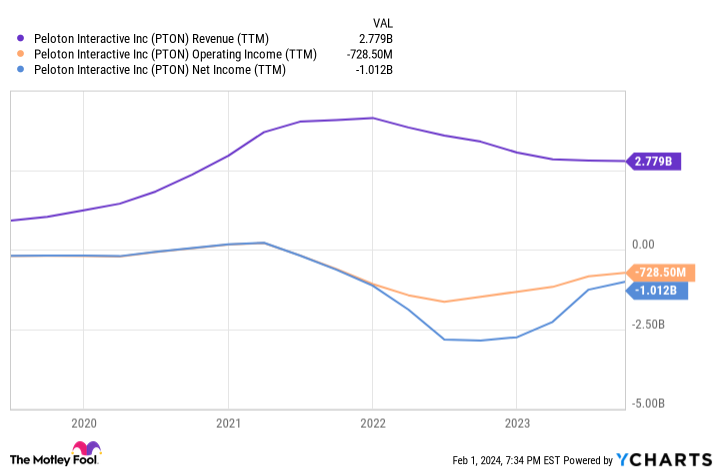

Yes, this is the same Peloton that just reported a 6% year-over-year slide in its fiscal second-quarter revenue, setting up more losses. Specifically, its Q2 top line of $744 million fell from the year-ago comparison of $793 million, leading to a loss of $195 million. That loss is smaller than the year-ago comparison.

Guidance for the fiscal third quarter now underway, however, is disappointing. The company only anticipates revenue of between $700 million and $725 million versus analysts’ consensus estimates of almost $754 million. With its ongoing existence now increasingly in question, the quarterly report and outlook shaved off more than 20% of Peloton stock’s value on Thursday of last week alone.

And yet, there’s a case to be made for taking a shot on Peloton’s (severely) beaten-down stock. Just make sure you understand the bet you’d be making. This isn’t a potential investment that’s right for everyone.

Peloton’s rags to riches back to rags story

On the off-chance you’re reading this and don’t already know, Peloton manufactures interactive fitness equipment like exercise bikes, treadmills, and rowing machines.

The business model is far more holistic, though. Its equipment is a means of selling consumers access to trainer-led online exercise sessions and app-based workouts. The integration of its fitness equipment and workout-centric digital media was a hit since it became an option.

But things went absolutely nuts during the COVID-19 pandemic. That’s when the world had plenty of time to exercise at home, and when more than a few people had access to stimulus money. As of the end of December the company boasted roughly 3 million paid connected-fitness subscribers, with another 718,000 users of its exercise app.

It wasn’t meant to last, however. As the world eased its way back to normal and lower-cost alternatives materialized, peoples’ interest in high-end fitness equipment — and exercising in general — waned. Peloton’s top line has been steadily sinking since 2021, and though its losses are now shrinking, they’re shrinking mostly because Peloton’s business is shrinking (thus crimping the company’s capacity to suffer losses).

Is there any hope for a rekindling of its previous growth? Never say never. The odds certainly don’t seem to favor it, though. Consumers’ commitment to their fitness goals is usually rather weak, and Peloton’s exercise equipment can be prohibitively expensive. Its exercise bikes start at a price point of over $1,000 apiece, for example, while its treadmills can cost as much as $6,000. Even more affluent consumers may not be interested in shelling out such sums for a piece of Peloton hardware, let alone a second piece.

In other words, don’t count on a turnaround anytime soon — if ever.

The curious bull case

And yet, there’s an unusual bullish argument to be made for stepping into the stock at its recently reached record low. Don’t misread the message. Buy-and-hold investors looking for easy-to-own, predictable stocks should search elsewhere.

If you can stomach some risk, though, here’s the deal: With a market capitalization of only $1.5 billion, the company’s shares already reflect worse than the worst case scenario.

OK, from a purely mathematical perspective that’s not quite the case. The company has $1.1 million worth of cash and inventory on its books plus another $140 million in receivables. That alone is very nearly worth $1.5 billion. Granted, it’s also got a little over $3 billion worth of debt and other liabilities on the books, making its technical liquidation value less than zero. (While some of that debt would be wiped out in the event of a bankruptcy, some of it wouldn’t.)

There’s another asset that doesn’t appear on Peloton’s balance sheet, though. That’s its powerful brand name.

Let’s face it. Although the business is struggling, Peloton is still the premier brand in connected fitness equipment — and the right organization could do something with it. The key is leveraging a large customer base to market the Peloton brand to, and then finding a way of making its fitness equipment more affordable to the masses. Apple has been floated as a prospective suitor.

That’s not a crazy idea, either. Apple’s iPhone is a premium-priced product, and its users are also more active users of paid apps and subscription-based content. They’re arguably Peloton Interactive’s top customer prospects.

And it’s certainly not like we haven’t seen similar moves before. Alphabet acquired then-struggling Fitbit back in 2021, for instance. Consumer goods outfit The Wonder Company completed its purchase of beleaguered meal kit brand Blue Apron late last year; it’s arguably able to do more with the brand than Blue Apron ever could have on its own. Wonder got Blue Apron for little more than a song too, paying only $103 million for the company that at one point said it was worth on the order of $3 billion.

Make no mistake about Peloton

So what’s the Peloton brand name worth to a potential acquirer? That’s tough to say. Maybe nothing. This uncertainty is why Peloton stock brings so much risk to the table. Indeed, betting on an acquisition may be even riskier than counting on a turnaround (although given the strength of the brand, nothing could ever be entirely ruled out).

Whatever the case, from a risk-versus-reward perspective the bulk of the risk here has already been wrung out of the stock’s price. What’s not being reflected is a brand name that still turns heads and commands respect. It wouldn’t take a whole lot to turn it into a healthy profit center for a larger player. A buyer may even be willing to pay a bit of a premium compared to today’s stock price for a shot at doing so.

Just keep your position size smaller than you normally might bite off, as a means of limiting your downside. This is still anything but your typical buy-and-hold-forever kind of pick, after all.

Should you invest $1,000 in Peloton Interactive right now?

Before you buy stock in Peloton Interactive, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Peloton Interactive wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of January 29, 2024

Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. James Brumley has positions in Alphabet. The Motley Fool has positions in and recommends Alphabet, Apple, and Peloton Interactive. The Motley Fool has a disclosure policy.

1 Growth Stock Down 97% to Buy Right Now was originally published by The Motley Fool